A lingering concern in the healthcare industry is the growing rate of insurance claim denials. Nearly one in four patients face claim denials, with insurance companies rendering their medical services as unnecessary. This poses a serious challenge to patients who have life-threatening/chronic illness and resolving denials based on medical necessity has become the need of the hour.

A rebuttal serves as evidence to refute or disprove an assertion made by the expert hired by the insurance company. This post will explore what rebuttal affidavits are and how they will prove to be useful in a medical litigation. Also, understand how a professional medical record retrieval team conducts thorough research to provide the evidence needed to strengthen the plaintiff’s position.

What Are Rebuttal Affidavits?

Rebuttal affidavit is a legal document drafted to counter the assumptions put forward by the opposing counsel, especially to expert opinions of insurance companies. These affidavits are vital in challenging insurance claim denials by presenting solid evidence and valid justifications. They provide structured and legally recognized ways to present counter arguments, thereby making sure that the plaintiff’s perspective is considered.

What Are the Different Types of Rebuttal Affidavits?

When you are going with a legal case in the medical industry, rebuttal affidavits are generally based on various subjects. These subjects are mentioned below.

- Investigations – Commonly includes: Pathology, Radiology, and other tests like CT Scans, Labs, etc.

- Allied Health Treatments: This can include Acupuncture, Physiotherapy, Occupational Therapy, and Chiropractic Treatment.

- Durable Medical Equipment or DME: This includes items like supporting TENS units, Braces, and other things.

- Surgical Intervention: This type will get you Corrective, Implant, and other surgeries.

- Injectable: Supporting procedures like Anesthesia.

These are the common types of affidavits that you can get, which are based on various subjects.

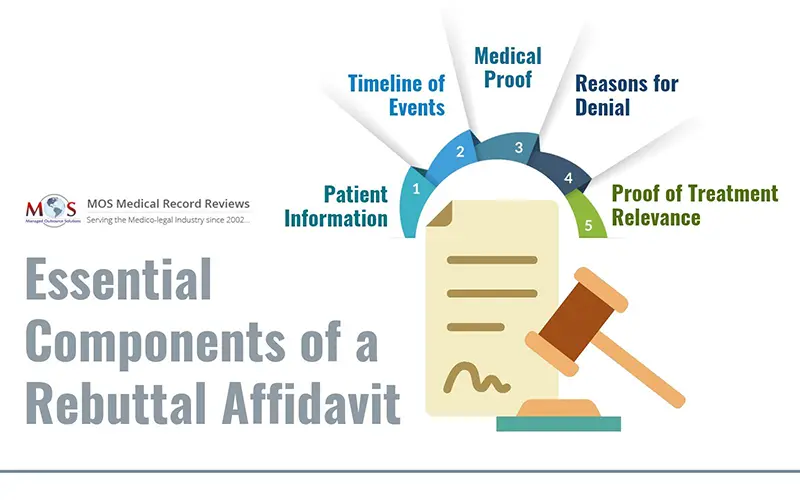

What Are the Essential Components of a Rebuttal Affidavit?

A thoroughly crafted rebuttal affidavit should include the following components:

- Patient Data: Mention the patient’s full name, policy coverage number, and the period of the denied claim.

- Medical Chronology: Make sure to present a comprehensive timeline of medical events related to the case.

- Evidence: Highlight documentation and medical records that will corroborate the legitimacy of the information and the claim.

- Denial Details: Make sure to include all reasons provided for the claim denial.

- Proof of Medical Necessity: Include all evidence regarding the necessity of the prescribed treatments and medications.

How to Write a Rebuttal Affidavit in Medical Litigation

The efficacy of a strong rebuttal depends on how well it is crafted and presented. Here are a few medical affidavit preparation tips for litigation:

- Accuracy: One of the most important aspects of a solid rebuttal affidavit has to be its accuracy of statements, to prevent discrepancies that could weaken credibility.

- Professional Tone: It is very important to maintain a respectful and formal tone, refraining from using accusatory or unprofessional language that could undermine your credibility in court.

- Extensive Research: Validate all presented claims through comprehensive research, including expert witnesses and medical literature.

- Relevance: Make sure to focus your attention on presenting information which is directly related to the case. Stray away from including extraneous details that could affect the purpose of the affidavit.

Drafting an effective rebuttal is not a straightforward task. Collaborating with an expert medical record review firm can help in preparing precise, concise and error-free rebuttal affidavits that can overturn claim denials in your favor.

What Is the Impact of Rebuttal Affidavits on Medical Litigation Outcomes?

When properly executed, rebuttal affidavits can help parties reinforce their arguments, thereby significantly influencing the trajectory of medical litigation in their favor:

- Reversing Claim Denials: A well-thought out affidavit can urge insurers to reevaluate and potentially overturn denied claims.

- Initiating Settlements: If your affidavit can present compelling counter arguments, it may foster out-of-court settlements, speeding up resolution and reducing litigation costs.

- Enhancing Case Merit: Well-structured affidavits contribute to the overall validity of the case, potentially turning judicial opinion in favor of the plaintiff.

Challenges in Preparing Rebuttal Affidavits

Considering the significance of these documents, drafting a rebuttal affidavit presents a series of challenges:

- Complex Medical Jargon: It requires experience and expertise to accurately translate intricate medical terminology into comprehensible language. Therefore, it is important to seek help on this matter.

- Access to Medical Records: It is very important to gain access to all pertinent medical records and documentation and the process can be arduous, but inevitable for a conclusive rebuttal.

- Time Constraints: Legal proceedings often work under strict deadlines, which drives for a prompt yet thorough preparation of affidavits, which could trigger unforced errors and compromise the presentation.

Final Thoughts

Rebuttal affidavits are indispensable tools in medical litigation for plaintiffs who are refuting insurance claim denials. These comprehensive documents dispute assertions made by defense experts, providing a seamless platform to present counter arguments and clarify complex medical issues.

By addressing the reasons—such as alleged lack of medical necessity—head-on, rebuttal affidavits solidify the plaintiff’s position, which can lead to the reversal of claim denials or initiate favorable settlements. Their strategic use ensures that legitimate claims receive due consideration, thereby upholding the integrity of the medical and legal process.

Looking to Draft a Compelling Rebuttal Affidavit?